With over 30,000 deal participants across 1,600 institutions using Termgrid, our platform sits at the center of the private capital ecosystem. To understand how investors, lenders, and advisors are navigating today’s climate, we surveyed the community on three themes shaping 2026:

- Market outlook

- Deal dynamics

- Technology adoption

The results reveal a market defined not by pessimism, but by uncertainty, resilience in the lower mid-market, and a decisive shift toward technology-driven efficiency.

Explore the full findings below to see how private capital is navigating change, and preparing for what’s next.

Please complete your details here to receive the full results by email. Or continue to read on the page below.

Who we heard from

Respondents were geographically balanced, with EMEA (48%) and the Americas (47%) accounting for the vast majority of responses. Participants represented sponsors, lenders, private credit funds, advisors, and other deal participants, spanning a wide range of fund sizes and strategies.

Market outlook: Neutrality replaces optimism

General outlook for private markets

Optimism has declined since mid-year, but negativity has also eased. This suggests that uncertainty, rather than outright pessimism, is weighing on sentiment.

When segmented by market size, a more constructive outlook emerges for the lower mid-market. In particular, 45% of respondents working with firms below $50mn EBITDA report a positive outlook, reflecting relative insulation from heightened competition, interest rate sensitivity, and broader macroeconomic pressures.

Fundraising environment: Challenging, but stabilising

While fundraising conditions remain challenging overall, there are early indications of a shift toward a more neutral or improving outlook, particularly in Europe.

Sentiment in the Americas remains more cautious, with over 40% of respondents continuing to view fundraising conditions negatively.

The outlook is notably more difficult for sponsors, where concerns persist among more than half of respondents. By contrast, sentiment among private credit funds is considerably more positive, with nearly 42% reporting an improved outlook.

Spread expectations: Flat to tighter, with segment differences

A clear majority (73%) of respondents expect spreads to tighten or remain flat over the next six months.

However, expectations diverge by segment:

- Sponsors (22%) and respondents working with firms below $100mn EBITDA (25%) expect spreads to widen

- This rises to 44% among those working with firms below $50mn EBITDA

These results point to greater pricing pressure at the smaller end of the market, even as broader sentiment remains stable.

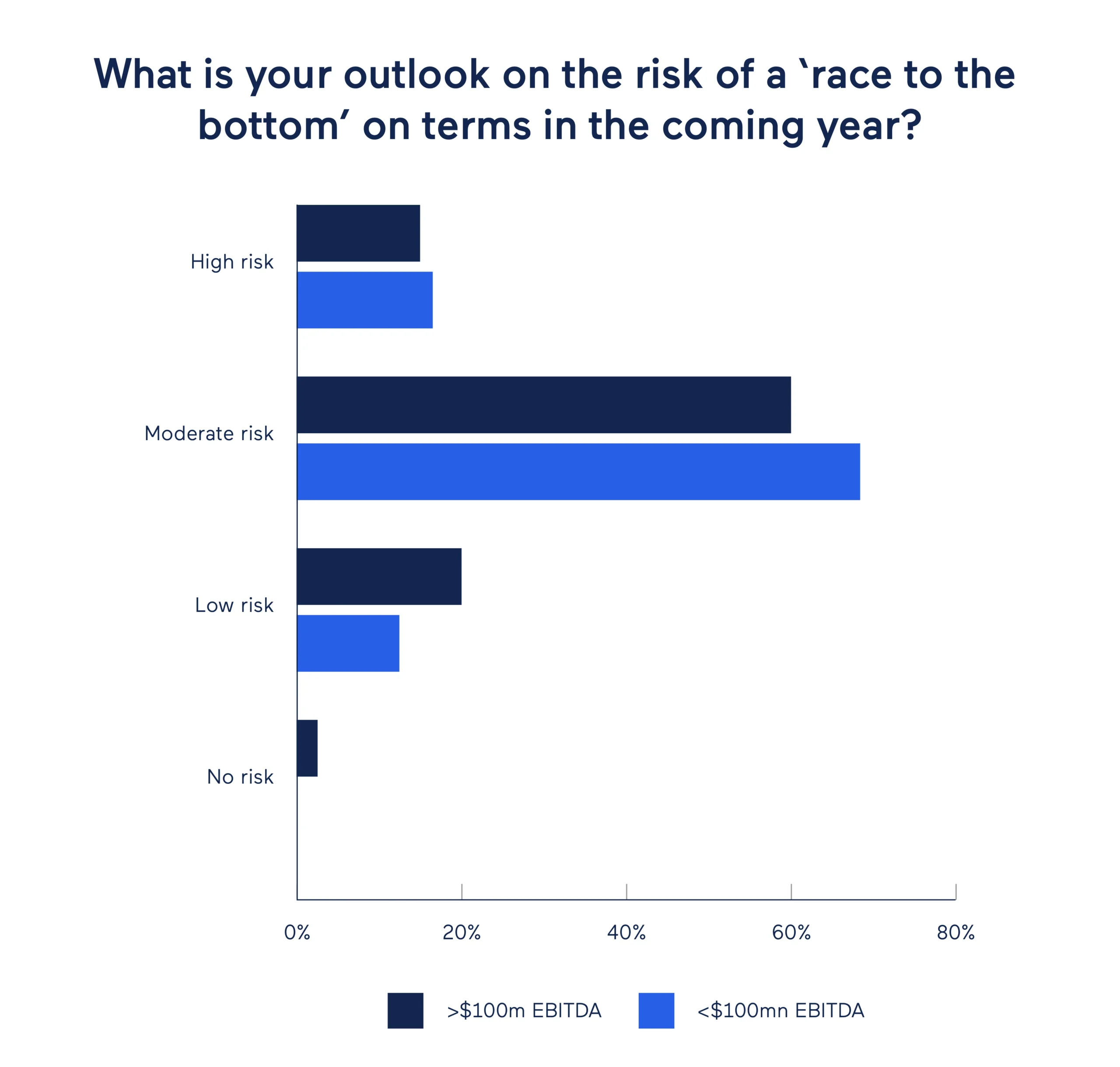

Deal dynamics: Race to the bottom risks & rising LMEs

Risk of a “Race to the Bottom” on Terms

Europe’s fragmented loan market has historically accommodated diverse documentation practices across jurisdictions and sectors. That tolerance, however, is being tested.

Survey responses indicate that European markets see a greater risk of a race to the bottom on terms compared to the Americas.

Notably, lower mid-market participants are relatively unconcerned, suggesting continued confidence in disciplined pricing and deal structures within this segment.

Liability Management Exercises (LMEs)

A majority of respondents expect the use of LMEs to increase over the next 12 months. This view is particularly pronounced among sponsors and advisors, and more widely held in the Americas (55%) than in EMEA (41%).

Technology: Efficiency gains drive adoption

Where technology can have the greatest impact

While virtual data rooms and online NDAs are seen as delivering the largest efficiency gains, respondents believe technology can improve efficiency across the entire deal process, including information sharing, relationship intelligence, and counterparty discovery.

Tracking deal terms: Moving beyond Excel

Early adopters are increasingly moving away from Excel toward purpose-built systems, driven by the need for data integrity, scalability, and real-time visibility. As deal volumes and complexity increase, spreadsheet-based workflows are proving less sustainable.

Barriers to adoption & realised benefits

Technology-driven efficiency is widely recognised, but implementation remains a challenge, particularly due to organisational policies and lack of time.

Among those who have adopted new technology, efficiency gains stand out as the most material benefit, ahead of automation, cost savings, and risk reduction.

Key Takeaways

- Market sentiment has softened, but uncertainty, not pessimism, dominates

- The lower mid-market remains comparatively resilient

- Fundraising is stabilising, with private credit more positive than sponsors

- Most expect spreads to remain flat or tighten, though pressure persists at smaller sizes

- LMEs are expected to increase, particularly in the Americas

- Technology adoption is accelerating, driven primarily by efficiency gains

About Termgrid

Termgrid is the market-leading software platform purpose-built for private capital markets. Trusted by 1,600+ institutions and 30,000+ users, Termgrid streamlines the end-to-end financing workflow, delivering efficiency and insight at every stage of a transaction.