At one time or another, every GP at a private equity firm has either kicked themselves for selling a portfolio company too soon, or been forced to sell a great company because a fund was winding down. This was simply the cyclical nature of the private equity business. Private equity firms raised a fund from limited partners, bought companies in those funds and then paid returns in 10 years time with the proceeds from selling the companies.

Times have changed. Today, private equity firms are more frequently forming single-asset continuation vehicles (CVs) to hold onto assets that they believe have more upside. CVs provide greater flexibility and long-term value for both general partners and limited partners. By offering extended hold periods, liquidity options, and the ability to align with market conditions, CVs allow private equity firms to optimize value. The growing popularity of CVs reflects a broader shift in private equity where strategies that deviate from the traditional private equity norms are becoming more widespread and acceptable.

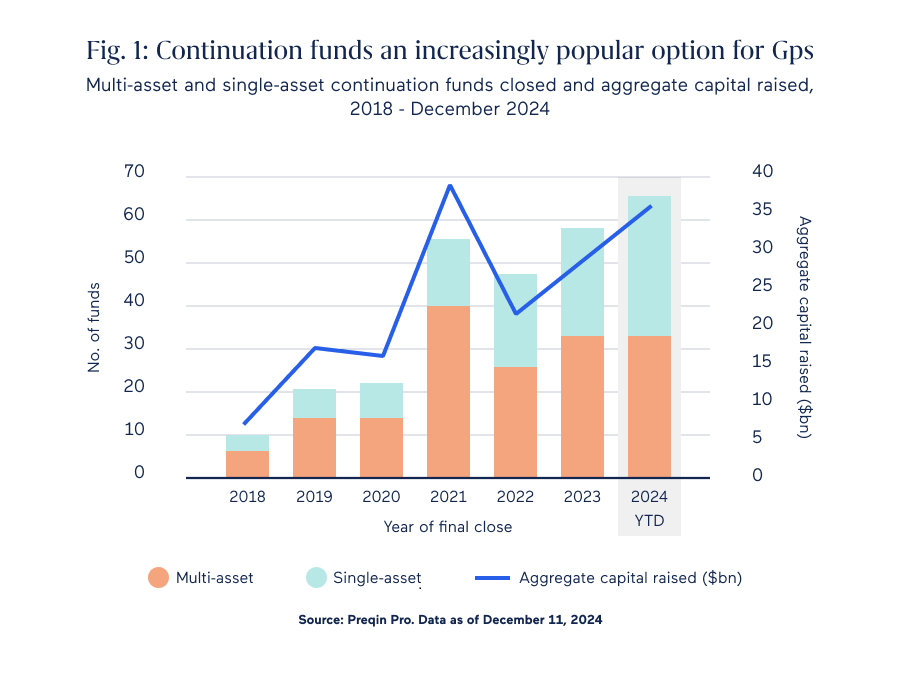

Private equity firms are certainly adopting the CV model. The single-asset CV market volume, in particular, is expected to double by 2028 to $51 billion, driven by new players and “innovative transaction structures,” according to investment bank PJT Partners.

The Riverside Company is increasingly using the strategy to hang on to winners in their portfolio as well. In 2017, the firm’s Australian Fund, The Riverside Australian Fund II, bought Energy Exemplar, a software utility business located in Melbourne. At the end of 2017, the company completed its first add-on acquisition of a company in Salt Lake City, Utah.

“We consolidated those businesses and grew them for a number of years. As we headed into 2020, when we were all stuck at home with COVID software companies were trading through the roof,” says Simon Feiglin, a managing partner with The Riverside Company and head of Riverside Australia. “RAF II was now late in its life cycle and we kind of stopped looking for add-ons because we didn’t have money left in that fund. As a result we were probably missing opportunities even though the company was performing exceptionally well.”

Simon Feiglin, managing partner at The Riverside Company (Image Source)

Even without add-on acquisitions the company continued to grow organically at about 30% per year. “The management company came to us and said, ‘We are growing, but there are add-ons we want to pursue.’ We were interested in continuing to support the company, but at the same time many of our investors wanted their money back,” says Feiglin.

In 2021, RAF II sold Energy Exemplar to a continuation vehicle, which ultimately sold the company to Blackstone and Vista Equity in May 2024. They were the first firm in Australia to complete an exit through a CV fund. “We were seeing extraordinary valuation in the software space and we decided the time was right for a sale,” says Feiglin.

When RAF II bought the business in 2017, the company was doing about A$20 million in recurring revenue. When Riverside’s continuation vehicle sold the business in 2024 the company was doing about A$140 million in revenue. “The continuation vehicle really gave us the time we needed to get the company on that growth trajectory. It was a great deal for everyone involved,” says Feiglin.

The Riverside Company is not alone in embracing the CV strategy. According to a report by Greenhill’s Global Secondary Market Review FY 2024, nearly 80% of GP-led transactions were CVs in 2024. “Five years ago, people didn’t understand them. They weren’t widely used. Today, they are prevalent,” says Feiglin.

Other private equity firms are using the option as well. For example, last year Hildred Capital raised $750 million to maintain ownership of Crown Laboratories and Hyland’s Naturals. Vestar Capital Partners raised a $1.2 billion single-asset continuation vehicle to continue to hold consumer analytics company Circana. Blackstone Strategic Partners and HarbourVest Partners acted as lead investors. And Apollo’s S3 secondaries arm led the $1.15 billion CV for OceanSound Partners’ engineering company SMX Group.

Alternative to secondaries

There are a few key reasons CVs have gained popularity. First, they are an alternative to secondary funds, which sells its stakes in a fund to a buyer blindly. When a GP goes to market with a CV they have the specifics of the underlying assets. This undoubtedly draws investors in. Continuation vehicles also provide a way for GPs to monetize their holdings or transition to new investors, offering a smoother transition for all stakeholders, including the management teams of portfolio companies.

Alti, an investment firm dedicated to creating private equity products available to accredited investors, is seeking to invest in continuation vehicles. “GPs are only going to roll their money with a company they have conviction in so there is great alignment of interest and LPs are usually investing on the same terms as the GPs so that leads to another alignment of interest. The economics are good, says Sheryl Schwartz, Chief Investment Officer, and Co-Founder of Alti. “Unlike when you co-invest, the GP already has a value creation plan in play. CVs may not return as much upside as the early days, but the loss rates are expected to be lower. It’s a good strategy.”

While the experts agree CVs are here to stay, market conditions can, and will, impact its popularity over time. “CVs should remain popular, but if various exit windows open up more, their use may reduce. However, they should continue to be a strong option at the moment for many and will be a tool in the toolbox going forward,” says Schwartz.

Feiglin agrees. “Firms will exit companies the best way they can. If the IPO market is hot, they will go public. The CV is another tool. It’s a logical tool for those investors who are willing to stay on the journey with you.”

Stay in touch with all of our latest updates and articles. Sign up now.