Merger and acquisition (M&A) activity has yet to make the eagerly anticipated rebound that investors have been awaiting for the past couple of years, but there is one sector that has remained in good shape. Healthcare is, literally, one of the healthiest portions of the M&A market –a trend that industry experts expect to continue for the foreseeable future.

Between an aging population and major changes in the ways that people consume healthcare, in addition to technology advancements that are rapidly altering the way that medicine is practiced, there is no shortage of factors attracting investors to the healthcare sector.

“There’s an inherent demand for healthcare that makes it an attractive market to invest in. Just think of it as a percentage of the GDP (gross domestic product), or from an employer’s perspective, where it is the number two cost behind salaries,” says Lenard Marcus, a general partner and the co-head of healthcare IT investments at Edison Partners.

“Our healthcare system has a lot of challenges… Whether it’s optimizing the care of a patient, the cost of providing care or the cost of drugs, there’s interoperability. But legacy systems don’t necessarily connect to one another,” says Marcus.

He notes that inefficiencies such as the inability of different components of the healthcare industry to efficiently exchange data have created attractive investment opportunities.

And technological advancements such as artificial intelligence are beginning to help to streamline many aspects of healthcare by creating new efficiencies –things as simple as doctors being able to dictate patient notes and files through simple transcription apps.

“We have seen AI show up in tech-enabled services such as imaging/radiology and in helping data companies pull insights out of unstructured data such as physician notes and discussions. Increasingly, it’s expected to play a bigger role in other tech-enabled services such as revenue cycle management and other business process automation,” says Rob Larson, a director at global strategy consulting firm Stax.

Boomers provide a healthy backdrop

Then there’s the fact that since 2011, each day roughly 10,000 Baby Boomers reach the age of 65, a pattern predicted to last through 2029. With healthcare costs increasing faster than the rate of inflation, coupled with such a large aging demographic —as of the 2020 Census, there were roughly 76.5 million Baby Boomers living in the U.S.— demand for healthcare will not let up anytime soon.

One particular offshoot that has emerged is services and technologies designed to assist aging in place, which enable people with failing health to live out their days in their own homes instead of having to move into assisted living facilities.

Soaring healthcare costs and the opportunities they create have not been overlooked by the investment community. Though overall M&A activity has been fairly subdued since its peak in 2021, the value of healthcare M&A actually recorded its second-highest year in 2024. Global healthcare M&A totaled $115 billion in 2024, representing the second highest total of deal value to date, according to Bain & Company.

Source: Bain report, Figure 6

A whopping 65% of that healthcare deal volume came from North America. Large deals were also a major driver of that increase, with five deals in particular accounting for $5 billion of total activity. Industry experts expect that the momentum will only continue to build throughout 2025.

“I do not see investment in healthcare slowing down. Look at what science has learned over the past few decades about improving lifespans and healthspans (the period of time that an individual spends in good health during their life). It’s remarkable, and it has led to some really interesting changes in the healthcare industry,” says Randi Mason, a partner at law firm Morrison Cohen.

She points to the fact that healthcare consumers traditionally had three places to access healthcare services or products –a doctor’s office, a hospital or a drug store, with costs paid either through health insurance or out of pocket.

Consumer access diversifies

As the healthcare industry has broadened, so too has the number of ways that people consume healthcare services.

Consumers can now access healthcare services in a myriad of ways, including med spas, concierge medical practices –where people pay a monthly or annual fee for a pre-determined service level, and countless products that purport to improve an individual’s health and healthspan.

“Not too long ago, healthspan wasn’t even a word that was part of the lexicon. But now you have nutrition and vitamins, sleep monitoring and devices to help you optimize all that, and I don’t see that abating,” says Mason. “It’s an area that’s relatively new, and those are all places where private investments stand to make a lot of money. So, I don’t think private investment will ease up there.”

Mason has already seen a noticeable uptick in companies gearing up for M&A deals, particularly on the sell side.

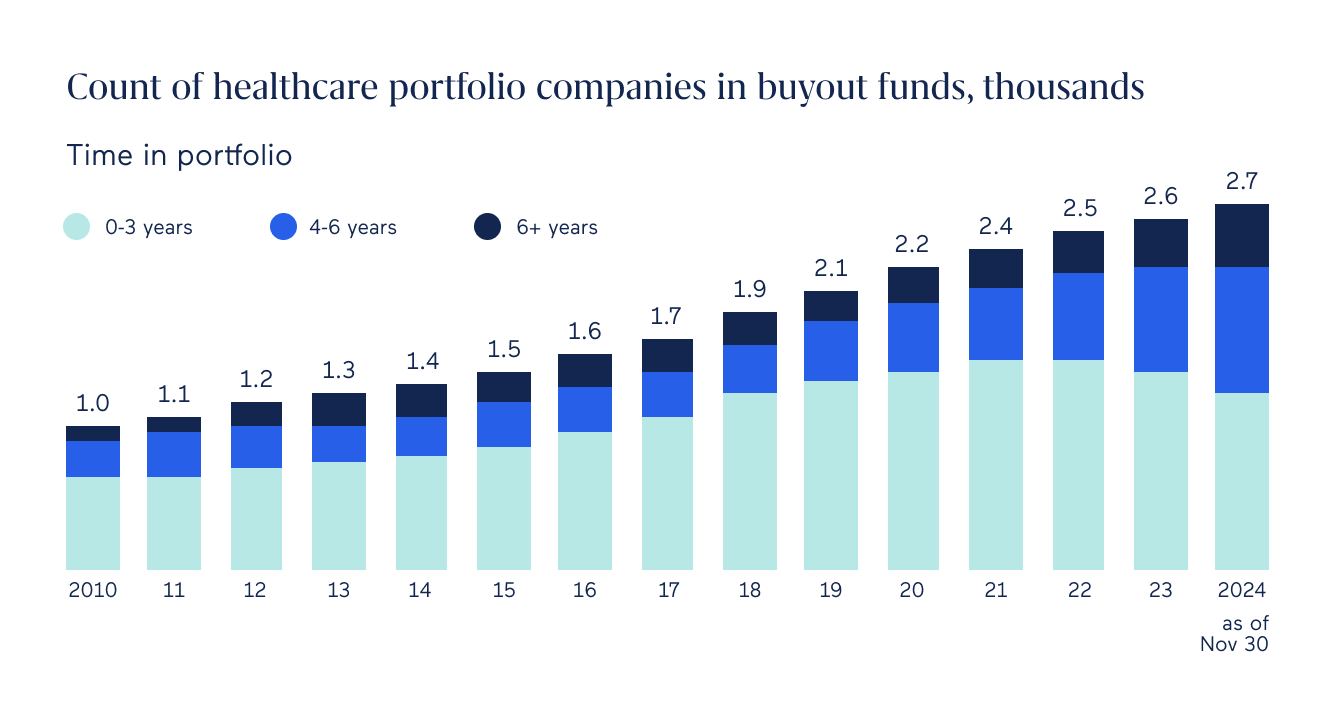

Though many PE firms have held on to portfolio companies far longer than intended in hopes of better multiples, she says there seems to be a sentiment that it is finally time to go to market, whether or not the desired multiples play out.

Where private equity investors may have pause is regarding some of the uncertainty that has been introduced by the Trump administration, particularly tariffs and the larger ramifications they could have.

“I strongly believe that this is the year the M&A floodgates will open, unless tariffs tank the economy and keep interest rates really high,” says Mason.

Adds Stax’s Larson: “There are a lot of healthcare assets in portfolio companies that need to be sold, and LPs are asking for their money to be returned before investing in a new fund, all of which suggests that deals are going to heat up compared to recent levels.

Political uncertainty pegs the sector

Overall political uncertainty is impacting the healthcare industry as a whole, as potential government cuts extend to everything from Medicare and Medicaid to medical research and trials and the president is decimating everything across the board.

“We’ve had cuts in various aspects of healthcare research and this will likely impact the investment dollars around clinical trial investments and other research related dollars.

Healthcare as a vertical will still be an attractive area of investment because the potential savings and ability to build a large impactful company will continue to persist. That said, there will always be legislative risks within healthcare,” says Edison Partners’ Marcus.

While there has yet to be a universal impact on a specific segment within healthcare, as people look at potential investments they’re going to have to study really hard or hire a third party to determine if there are any legislative risks,” says Marcus.

Adds Mason: “Sometimes the government invests in things that are not profitable, but which are necessary. Whereas the private sector only tends to invest in things that are profitable. Elon Musk is all about privatization, so I can see a lot getting driven into the private sector.”

One area where federal job eliminations could have a detrimental impact on investments in healthcare investing is venture capital, where many venture funds have invested in early state technology companies that license software or devices that have been patented by the government. In the wake of massive federal job eliminations, if the people who oversee the licensing of such medical technologies are impacted it could slow the pipeline of opportunities that would otherwise be marketed to private equity investors.

Valuations are another area of uncertainty. Industry experts note that valuations for healthcare deals have been more aggressive than they were four to six quarters ago, when there were still widespread macroeconomic doubts about the future.

With the consensus favoring a soft landing, until now, healthcare deals have had some of the strongest and most aggressive valuations compared to other sectors. But if tariffs have a negative impact on leverage and interest rates, things could change on this front as well.

“We’ve seen multiples in the single digits for either lower-quality or retail-heavy assets, and multiples in the 20’s for high-quality assets,” says Stax’s Larson. “There has been more of a focus on high-quality assets on the part of buyers, so that middle-tier and lower-quality assets aren’t getting as high multiples now as they did a few years ago, while the highest quality assets are trading at very high prices.”

Another shift he has noticed is the emergence of more middle market investors and a greater willingness on their part to extend down into the lower end of the market in the search for deals.

For now, there is optimism that healthcare deals will remain in demand and that activity will continue ramping up. “I’m seeing some of the best deals we’ve seen in a while. They run the gamut from data and interoperability to prior authorization technologies, and we’re seeing a lot of new entrants on the senior care side. And what’s most interesting is that many series A fundings have been wise and reduced their costs, so they are telling better stories when it comes to their ability to deploy capital and their near-term return on investment,” says Marcus.

Stay in touch with all of our latest updates and articles. Sign up now.