While listing activity has started to pick up and there is some expectation that this will gather pace in the new year, market participants point to a perceived lack of liquidity in the public markets as a particular problem for many companies in the technology sector.

“Below a certain threshold, institutional investors are not prepared to invest in the quoted market, and this is driving a lot of public to private deals,” the European technology banker says. “Stock markets are not really servicing smaller mid-cap companies very well. Valuations go down, and there is no buy-side interest from traditional stock market investors, and this is where private equity pounces.”

And while some of the sector’s biggest deals so far this year have included public to private (P2P) transactions like technology-focused private equity group Thoma Bravo’s $5.3bn acquisition of cybersecurity Darktrace, state-backed French lottery operator Française des Jeux’s €2.6bn ($2.8bn) acquisition of Stockholm-listed gambling group Kindred and the completion in October of an EQT-led £2.2bn ($2.8bn) acquisition of AIM and London-listed video games and entertainment technology provider Keyword Studios, few believe there has been a remarkable trend in the more active mid-market towards P2P activity.

Buyer growth expectations, one technology sector adviser says, are not always being met. And it is this which is at the heart of the dilemma for tech investments. A sector that has traditionally been sold on growth potential alone now needs to have a more compelling story.

The extent to which growth, or the perceived lack thereof, has been holding back technology transactions can be better seen in the much more active private markets.

Growth has been particularly difficult for the IT services sector, whose companies are often more exposed to cuts businesses feel they have to make in their discretionary spending.

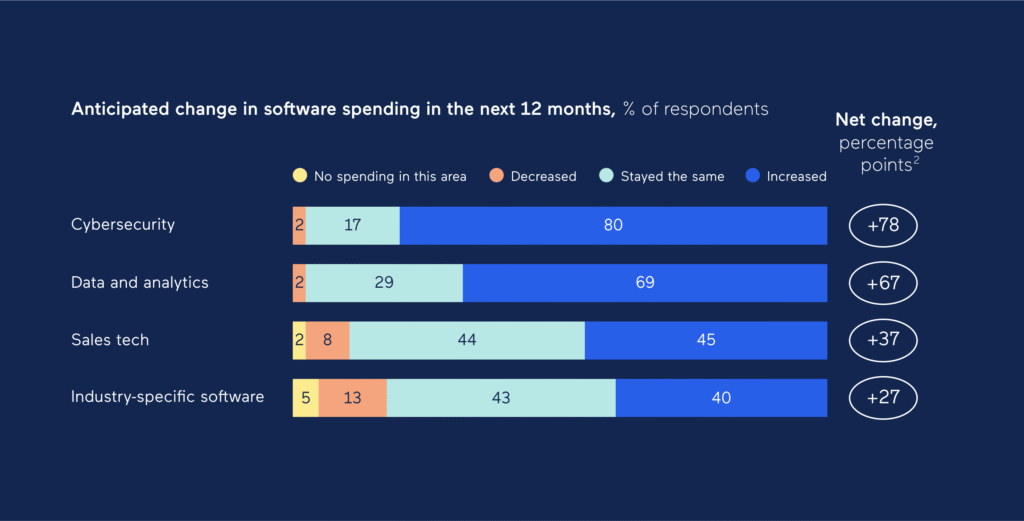

While the macroeconomic environment has undoubtedly weighed on overall spend, it would be easy to miss the nuances among the headline figures. A McKinsey report suggests CIOs are still expecting to increase overall spend on IT, with cybersecurity, data and analytics, sales tech, and industry-specific software showing the biggest increases.