This insight is drawn from a seminal study of private debt funds completed by Joern Block and Anna Schulze of the University of Trier and Young Soo Jang and Steven Kaplan of the University of Chicago Booth School of Business.

The study was conducted in 2021 and completed in 2023.

US investors largely rely on sponsors for their dealflow while European investors source from both sponsors and independently. This finding is based upon first hand responses from private debt funds in both regions and shows that U.S funds invest significantly more of their capital in PE-sponsored deals, 78%, compared to European funds at 41%.

The study also looked at the factors taken into account as part of the investment decision. It found that while stable cash flows play an important role on both sides of the Atlantic, there are differences in priorities.

US managers prioritize stable cash flows over the management team and business model (although the management team is also important to them), whereas European managers are more like PE investors and consider the management team, stable cash flows, and business model to be roughly equally important.

According to the authors, the two findings may be related. The presence of private equity sponsors in US deals may exert a stabilizing influence on these companies and provide comfort on any questions relating to management or the business.

The study goes on to look at the relationships between private equity sponsors and debt investors. Investors – particularly in the US – find that the presence of a sponsor helps with deal quality and deal sourcing.

It also helps with reduced costs. Sponsors and lenders build relationships based upon multiple interactions. Which results in more effective covenants and a willingness to lend at higher multiples.

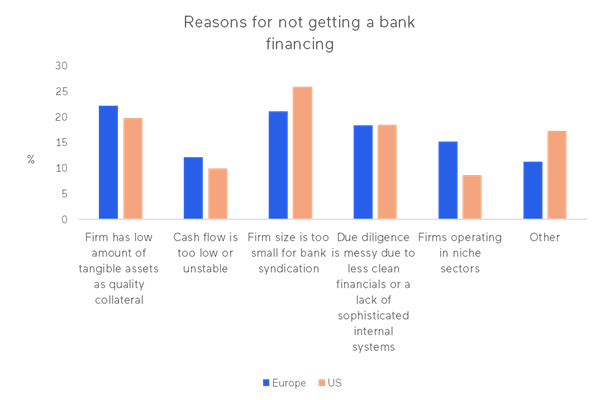

This is an extremely valuable study which reflects first person responses from the private debt community. Among the many other findings in the study, it goes on to look at the valuable role that private debt plays – including providing financing where companies may not be able to access bank financing.