The image of a swan gliding atop the water is peaceful and tranquil, but below the surface the bird is paddling its feet at a rate between 1.5 and 3 miles per hour. Much like a gliding swan’s grace disguises the amount of work its feet are doing, there is a lot more going on beneath the surface of the world of venture debt than it would appear.

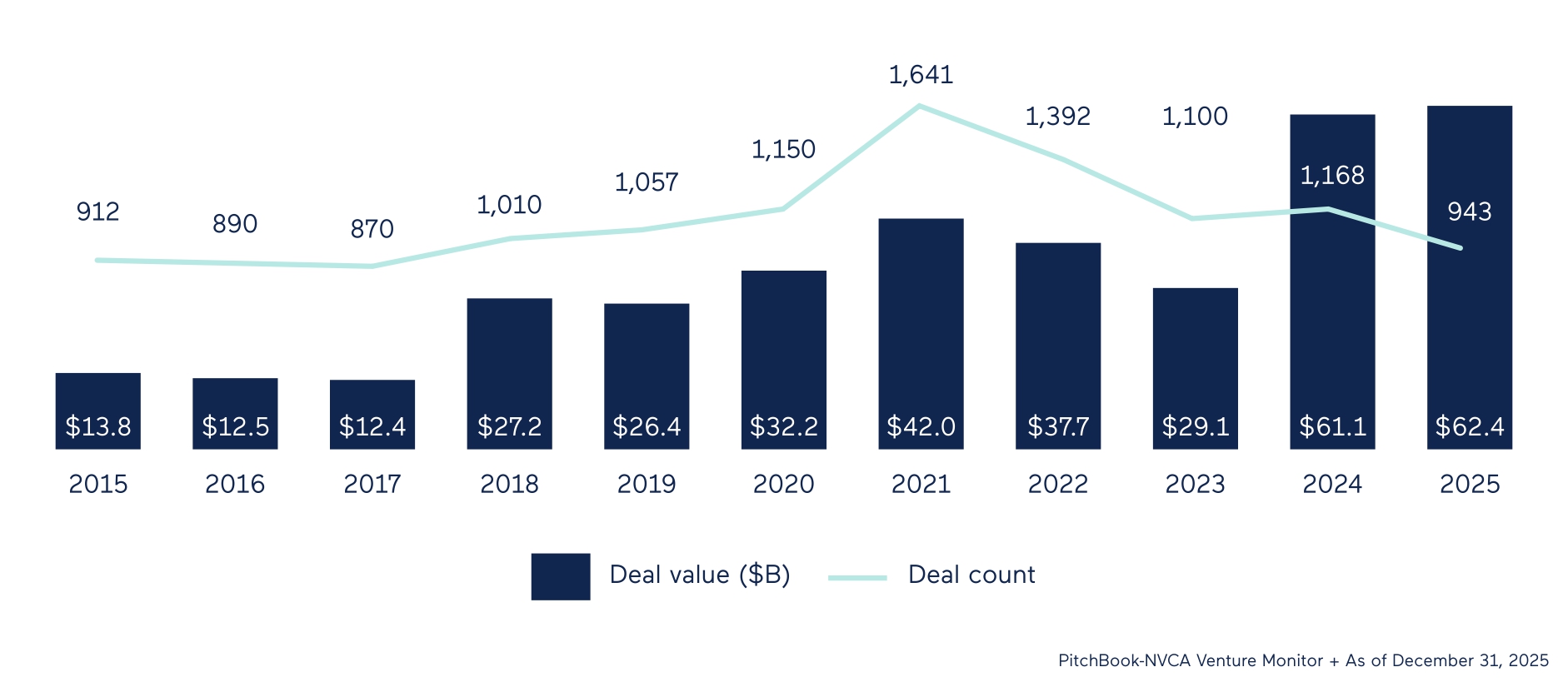

Venture debt lending has soared in recent years, with 2025 deals totaling a record $62.4 billion in 2025 – momentum that has continued so far in 2026.

But while lending activity remains strong, there has been a shift in the companies that lenders find appealing.

Artificial intelligence (AI) is a major determinant of which companies lenders will back, with capital chasing AI deals, but eschewing many of the technology companies — particularly software as a service (SaaS) — that previously comprised the bulk of deals in this area.

Larger deals also account for a major portion of venture lending activity. And though venture debt lending activity remains strong, there has also been a significant uptick in the number of defaults within the sector, a trend that industry participants predict will remain ongoing for the foreseeable future.

AI reshaping lending decisions

“Given the AI and software uncertainty, a lot of venture debt is sort of on pause right now as folks weigh the ramification of some of the AI implications to these companies,” says Peter G. Williams, a partner at law firm Cahill Gordon & Reindel and co-head of its private credit practice.

He notes that AI, specifically uncertainty regarding the risk of competitive disruption, has spurred many venture debt lenders to take a wait-and-see approach regarding software companies that were previously prime venture debt candidates. One particular concern he points to is the lack of clarity regarding valuation multiples and other assumptions for these companies that were considered tried and true just a year or so ago.

Venture debt is appealing to investors because it provides high-yield income through companies that have already received initial capital investments from venture capital firms. In recent years, venture debt investments have largely gone to technology, fintech and SaaS companies, all of which offer promising growth potential but need capital to support their growth.

But Pete Mathias, the founder of Reveille Venture Capital, believes there is a shift taking place. He points to a broader macro push toward reindustrialization, including energy, aerospace and defense, and AI infrastructure such as data centers and semiconductors.

He adds that uncertainty around AI’s impact on intangible, software-driven businesses is pushing investors toward companies with more tangible, asset-backed value. As AI continues to erode competitive moats, investors are increasingly focused on how defensible an asset truly is and how quickly AI could disrupt it.

Rising risks, defaults, and market stress

AI is also expected to reduce competition among lenders, as some participants step back, allowing more specialized venture lenders to be more selective.

At the same time, risks are rising. Industry participants point to geopolitical uncertainty — including conflicts and policy shifts — as well as broader systemic risks that could disproportionately affect venture debt compared to asset-backed lending.

Defaults are already increasing, according to Zach Ellison of Applied Real Intelligence (A.P.I.), who notes that many troubled loans are being quietly restructured rather than formally marked as distressed. Lenders are extending terms and amending agreements, masking the true scale of the issue.

Jennifer Post of Thompson Coburn highlights that more than half of venture debt capital is now chasing AI deals, putting pressure on traditional SaaS and software borrowers. These companies are increasingly seeking covenant relief, payment extensions, and other accommodations as they struggle to compete.

She adds that many of the most stressed companies were funded 18 to 36 months ago and are now unable to achieve prior valuations, though stakeholders are often reluctant to accept these lower valuations.

A market reset and return to discipline

Aarondeep Bains of Aird Berlis has also observed rising defaults and notes that some lenders have been “kicking the can down the road” by modifying deal terms. He also highlights a geographic shift, with some Canadian startups relocating or restructuring in the U.S. due to political and funding concerns.

Despite these challenges, overall deal activity remains strong. However, lenders are responding to uncertainty by tightening deal terms.

“Deals have covenants, restrictions and more strenuous reporting… it’s kind of a return to normalcy,” says Bains.

The venture debt market is increasingly moving back toward pre-pandemic discipline, with stricter underwriting, tighter structures, and a more cautious approach likely to define the path forward.